Table of Contents

Introduction

This is the first in what I intend to be a short series on equity. I’ve found that for many tech startup employees, equity is the least understood part of the compensation package. Meanwhile, it has the potential to create the largest value for the employee. It is crucial to understand what startup equity is, how it works, why it is awarded and what it can become.

I’ve found that case studies are an incredibly effective way to make a concept salient. So I’ll be using them in this series. Our focus will be a hypothetical company called Zarona that has employed a product manager named Bassey.

Knowledge Check #1

Let’s start with a quick quiz. The answer will be at the bottom of this article.

Which of the following statements about stock options is TRUE?

a. Stock options give me dividends while I’m employed

b. If I leave the company before my options vest, I can still exercise them

c. Stock options give me the right to buy shares at a fixed price in the future

d. Once granted, options are immediately mine to sell

Key Terms

Equity: Ownership in the company, giving you a stake in its success.

Stock Option: The right to buy company shares at a fixed price (called the “strike price”).

Share: A unit of ownership in a company.

Restricted Stock Unit (RSU): A promise of shares, granted once certain conditions (like time or performance) are met.

Equity Grant Agreement: A legal document detailing the number of shares you’re granted, vesting terms, and type of equity.

Cap Table (Capitalization Table): A record of all shareholders and how much of the company each person owns.

Vesting: Earning your equity over time or based on milestones (time-based, event-based, or hybrid).

Exercising: Buying your stock options at the grant/strike price, converting them into actual shares.

Grant/Strike price: The fixed price at which you can buy each share of the company, regardless of how much the company grows or how much its shares are worth later.

83(b) Election: A tax move that lets you pay early when your equity value is low—potentially saving a lot later.

IPO (Initial Public Offering): When the company goes public and you can sell your shares on the stock market.

M&A (Mergers & Acquisitions): When the company is sold or merged; your shares may be bought or converted.

Tender Offer: When the company or investors offer to buy back your shares before an IPO or exit.

Secondary Sale: When you sell your shares to another person or investor, instead of the company issuing new shares.

ISOs (Incentive Stock Option): A type of stock option for employees that may qualify for special tax benefits under U.S. tax law if certain conditions are met.

NSOs (Non-Qualified Stock Option): A type of stock option that does not qualify for special tax treatment. It is subject to ordinary income tax upon exercise.

PTEP (Post Termination Exercise Period): The window of time an employee has to exercise their vested stock options after they leave (or are terminated from) the company.

AMT (Alternative Minimum Tax): A parallel tax system that ensures people with certain benefits (like ISOs) still pay a minimum level of tax.

Capital Gains: Capital Gains are the profits you earn when you sell an asset (like shares) for more than you paid for it.

Equity Explained

Equity = Ownership

Simply put, having equity in a company means that you own or are earning the right to own a piece of the company. There are two common types of equity:

1. Stock Options – The right to buy shares of the company in the future, at a set price.

2. Restricted Stock Units (RSUs) – The promise of shares granted once certain conditions, like time, are met.

Because stock options are a little more complex than RSUs, for this series, as the title indicates, we’ll focus on options.

An equity grant is an incredible job perk. It is the potential to own a piece of a company, which, if trending in the right direction, can create life-changing wealth. Typically, if you’re being granted stock options as part of a compensation package, you’ll receive an equity grant agreement. This is a personalized contract that tells you how many options you have, what type they are (ISOs vs NSOs) and your vesting schedule.

Vesting = Earning your options over time

Options are typically subject to a vesting period and for good reason. Having a vesting schedule promotes and rewards loyalty, as employees earn portions of their right to own part of the company, as they commit time to building the company.

It’s a standard practice for options to vest over 4 years. Usually, there will be a cliff – a period during which no options vest and after which options begin to vest on a set timeline. This cliff may be a few months, but it is usually a year.

So, if Bassey was awarded an option grant with a 1-year cliff and 4-year vest, he will earn zero options in year one and on the first day of year two, will earn 25% of his options.

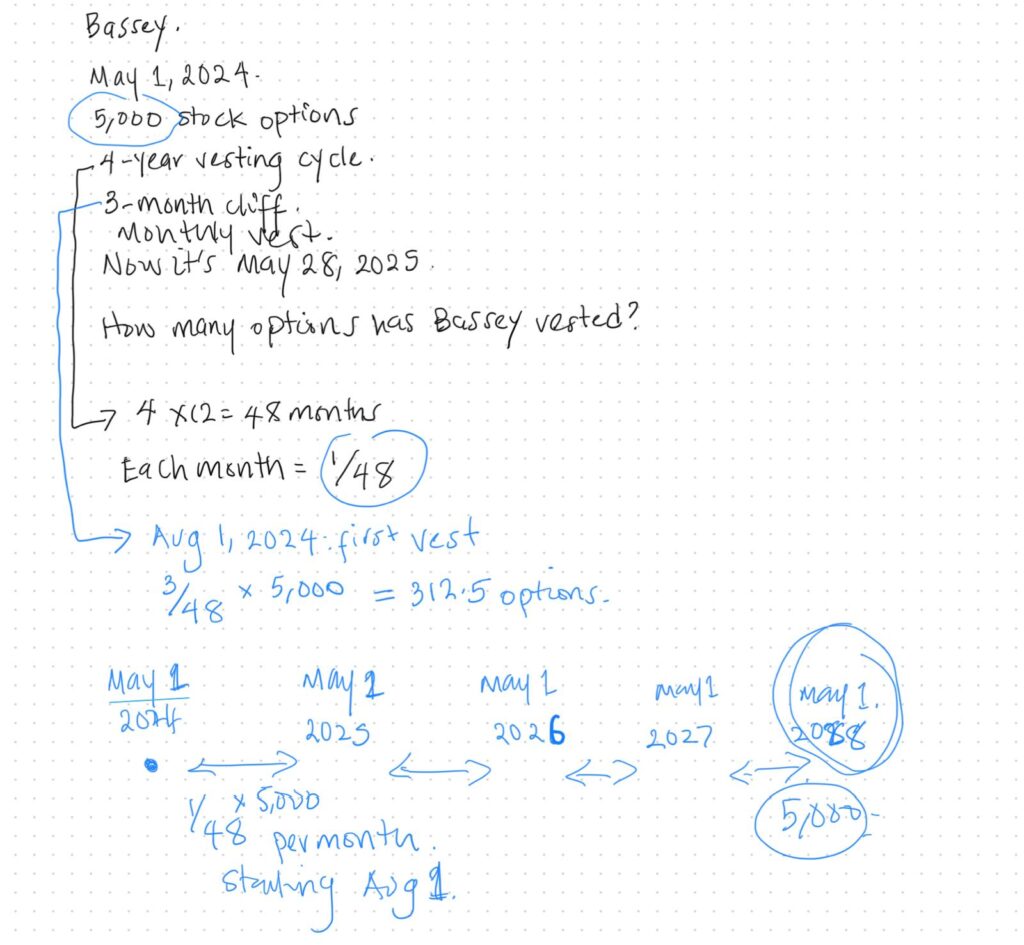

Now imagine Bassey was awarded 5,000 stock options on May 1, 2024, subject to a 4-year vest and 3-month cliff. It is now May 28, 2025; how many options has Bassey vested?

You can see that Bassey would have vested 1/48 times 5,000 options per month starting August 1, 2024, in addition to the 312.5 options that vested at once in that first vest.

There are 9 months between August 1, 2024 and May 28, 2025. So 9/48 times 5,000 = 937.5 options.

Which means that by May 28, 2025, he would have vested 312.5 + 937.5 = 1,250 options.

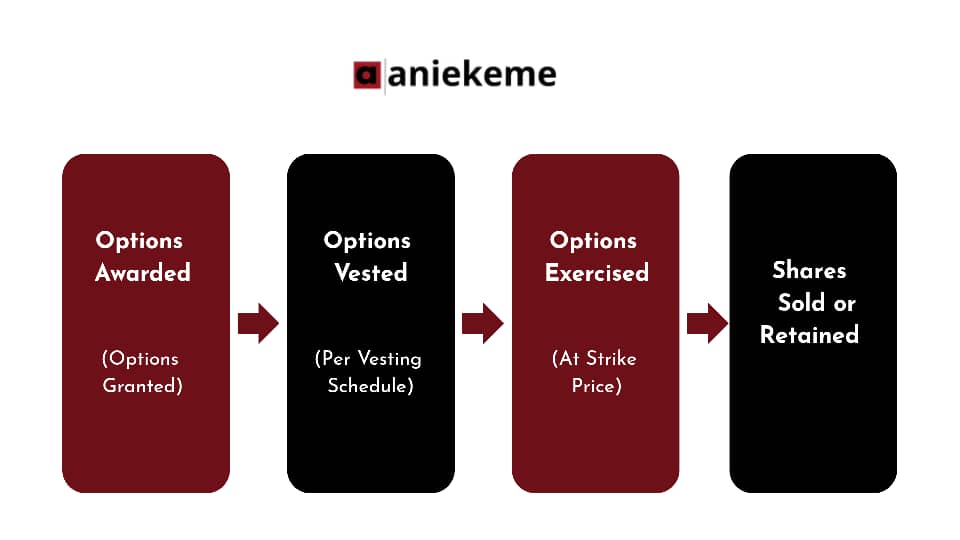

Exercising Your Equity

To “exercise” means to buy your shares. Once your options vest, you can choose to buy them. It’s important to know here that vesting your options does not mean you now own shares in the company. It is only by exercising your options, aka buying your shares at the strike price, that you then have gained ownership in the company.

You can only exercise after vesting.

You only own after exercising.

Most companies have a window within which employees can exercise their options if they choose to leave or are terminated from the company. This window is called the Post Termination Exercise Period (PTEP) and varies from company to company with the shortest and most common being 90 days and some of the longest being up to 7 years (reportedly at Pinterest) and 10 years (reportedly at Loom).

Knowledge Check #2

Let’s see how you’re tracking with a quick quiz. The answer will be at the bottom of this article.

What does it mean to ‘vest’ your options?

a. You can sell them immediately

b. You now own the right to exercise that portion

c. You are eligible for dividends

d. The company is required to buy them back

Equity and Taxes

Can we discuss money without discussing taxes?

I’ll keep this section brief though, because with these sorts of matters, it is best to consult with a tax expert, as there might be nuances based on your citizenship and taxes and tax treaties are subject to change.

The most important thing to know when it comes to equity and taxes is that when you sell your shares for more than you paid for them, you generate what is called a capital gain. Capital gains may be short-term (if you sell less than a year after exercising) and long-term (if you sell more than a year after exercising). And capital gains usually have their own tax rates, generally 30% in the U.S. and 10% in Nigeria.

So after you exercise and sell your shares, you may be subject to this capital gains tax. My understanding so far is that in Nigeria, the gains from the disposal of shares are exempt from capital gains tax. Consult a tax expert before making any exercise or sell decision.

How Equity Becomes Money

Your equity becomes real money during certain company milestones. There are three main ones:

1. Initial Public Offering (IPO): the company goes public and you can sell your shares on the open market.

2. Merger or Acquisition (M&A): the company is acquired or merges with another company and you receive a cash-out for your shares.

3. Tender Offer or Secondary Sale: the company or investors may offer to buy your shares, usually during a funding round but also could happen at any time.

Equity in Action

Back to Bassey and his 5,000 stock options awarded on May 1, 2024, subject to a 4-year vest and 3-month cliff.

Let’s assume that he was granted these options at a strike price of $1.

By June 2, 2028, Zarona’s value has grown to $10 per share.

By this point, Bassey has fully vested his 5,000 options and decides to exercise them. He would pay:

$1 x 5,000 = $5,000

Now he owns those 5,000 shares and can sell them:

$10 x 5,000 = $50,000

And his gross gain would be:

$50,000-$5,000 = $45,000

In Summary

Knowledge Check #3

Let’s say you were also employed by Zarona and granted 1,000 options with a $1.20 strike price. If Zarona exits at a $10.00/share valuation. You are fully vested and you exercise and sell all options at exit. What would your gross gain be?

a. $1,200

b. $8,800

c. $10,000

d. $0 (I wouldn’t profit until the shares increase in value again)

Some additional things to know:

+ You can sell your shares during a secondary sale without paying to exercise. This is called a sell-to-cover. You sell at the current valuation/share price and your proceeds are less the strike price (and fees). So in a sell-to-cover, you don’t need to lay out your own cash in the transaction.

+ An employee may be able to vest options even upon exit from the company if the employee’s agreement includes a clause on accelerated vesting. This is quite uncommon, but does sometimes happen.

I hope this has been helpful! Looking forward to the next entry in this series on equity.

Warmly,

Aniekeme

Answers:

Knowledge Check #1: c

Knowledge Check #2: b

Knowledge Check #3: b